The CBDT has apparently directed the officials of the income-tax department to “go into overdrive” in the next three months while making recovery of tax. The officials have been warned that their performance is being “monitored at the highest level“.

According to a report in the ET, the income-tax department is expected to go into overdrive in the next three months with the Central Board of Direct Taxes, the apex body, alerting all senior tax officials that their performance is being “monitored at the highest level.”

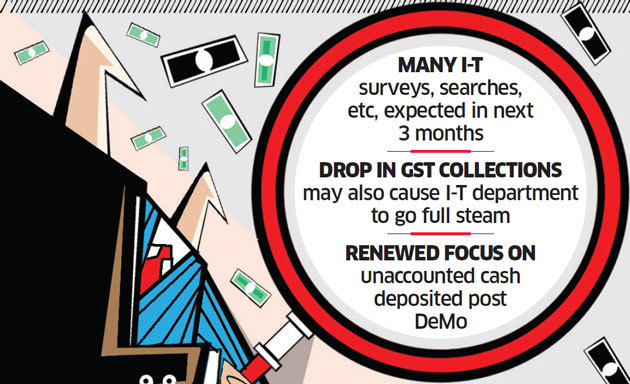

Many searches, surveys etc

“There will be searches, surveys, information verification, and follow-ups. Explanations on ‘cash in hand’ amounts are being sought from different kinds of assessees, and not just from large establishments and jewellers… We will be knocking on many doors even if our respective targets are met,” a senior tax officer was quoted as saying.

The CBDT Chief apparently conveyed this message to the tax officials during a recent video-conference.

(Image credit: ET)

It will also give a renewed push towards imposing and recovering tax on Rs 3 lakh crore deposit, which is suspected to be the quantum of unexplained cash parked with banks post demonetisation.

It was also claimed that the drop in GST collection following cut in tax rates and refunds have prompted the CBDT to direct tax offices to go full steam ahead.

Slowdown in refunds, high-demand appeals to be fast-tracked

“A possible slowdown in income tax refund, directing the CIT Appeal to dispose of appeals confirming the additions, investigating cases where assesses have deposited more than Rs 10 lakh in demonetised notes may push up gross collection. But does this really reflect the true state of tax collection in a slowing economy where the GDP growth rate is admitted to have come down,” a chartered accountant was quoted as saying.

It is also stated that in some of the large tax collection zones like Mumbai, the Chief Commissioners have directed Commissioner of Income-tax (Appeals) to dispose of high-demand appeals before the close of the financial year.

About two months ago, tax offices were directed to accept only those revised tax returns where there is a “bonafide inadvertent error” or “a mistake” on the part of the assessee. This was to tax the unaccounted cash that was deposited after demonetisation (of high denomination currency bills in November 2016) and subsequently regularised through a revised return and payment of tax on it at the normal rate of 30%.

Principal CIT & ACIT fined Rs. Rs.50,000 each for illegal tax recovery

It may be recalled that in ACIT vs. Epson India Pvt. Ltd the Karnataka High Court has recently passed severe strictures against the Income-tax department for raising high-pitched and unsustainable demands.

“First raising unsustainable, illegal and high pitched demands and then seeking to coercively recover the same even showing scant regard to the orders passed by highest Tribunal under the Act and for that invoking the writ jurisdiction to seek support to their such effort is nothing but an utterly irresponsible and unfair behaviour. It is the lack of such discipline with the Government Officials which turns Government Departments as a major litigant in the Constitutional Courts, in turn depriving the Constitutional Courts to devote their time for looking into the causes of poor people, which deserve their time and attention of the court more than such Government Department,” the High Court.

Yogesh Pande, the Principal Commissioner of Income Tax-2, Bengaluru, and Preeth Ganapathy, the Assistant Commissioner of Income Tax, Circle-2 (1)(2), Bengaluru, were directed to pay Rs. 50,000 each from their personal resources for harassing the assessee and wasting the time of the Court by filing the frivolous writ petition.

However, the strictures passed by the High Court are unlikely to deter the department in pursuing their high-handed approach towards tax recovery.

Leave a Reply